UK 2Q Economy: Even the Vultures Look Pinched

A predatory profits model is picking over the bones

I am sorry to inflict more economics on you, but the details of 2Q’s national accounts published on Friday house an explanation of how and why we are failing, the scope of the challenge now before us, and the origins of the ‘cost of living crisis’. I think it is important that you know how this is (not) working.

The ‘cost of living crisis’ is, in effect, the point at which Britain’s profits model (historically and geographically unusual) is exhausting its raw material - which is you and me.

Any profits model which depends on household and government dissaving, must eventually reduce the population and its government to beggary. And there’s precious little profit to be had from beggars. The evidence from 2Q22 is that we are finally reaching that point.

However, if your profits are derived principally from household dissaving, then when your business encounters unexpected problems (war, drought, lack of confidence) your reflex response will be that households will just have to be fleeced that little bit more closely. It’s what you know. Which is why all manner of companies are jumping at the chance to raise their prices outrageously.

Only a radical re-imagining of Britain’s corporate and social culture will be able to start a rescue. To date, no major political party has the imagination to attempt it, or the guts. But it will happen eventually, because it must.

This piece uses the Kalecki profits identity which recognizes that corporate profits can only come from i) net investment; ii) net h’hold saving/dissaving; iii) net government saving/dissaving and iv) net exports. This equation is not controversial or eccentric: indeed, it is the basis upon which the US Bureau of Economic Analysis tracks US profits.

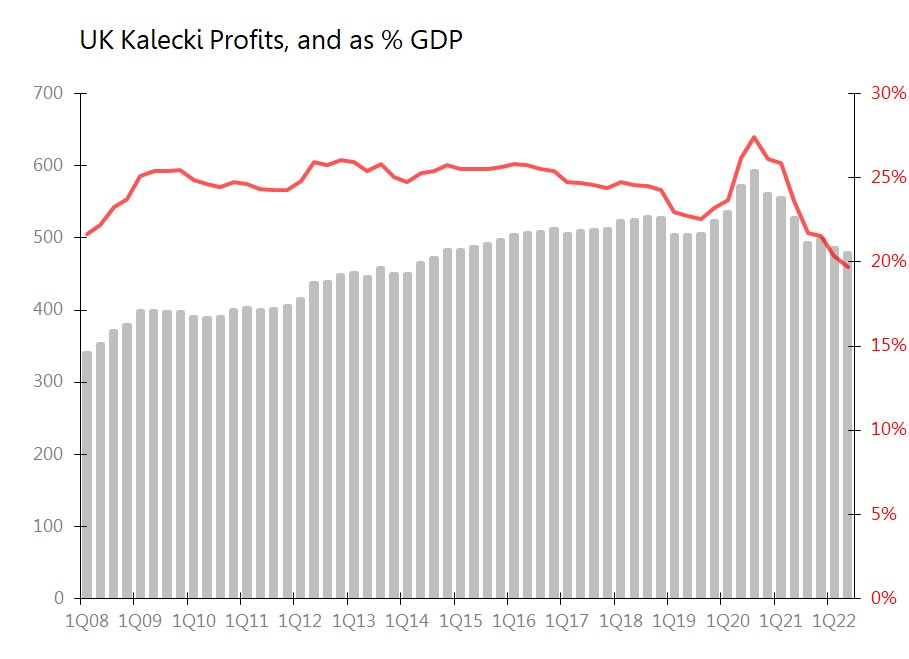

From the initial estimate of 2Q GDP, this equation results in Kalecki profits falling 1.3% qoq in the 12m to June, and falling 9.2% yoy. At £479.2bn, those profits are equivalent to 19.7% of GDP. This is the lowest Kalecki profits/GDP result this century so far. As the chart shows, profits have been falling almost consistently since their peak in 3Q20, and in nominal terms are now at their lowest since 3Q14.

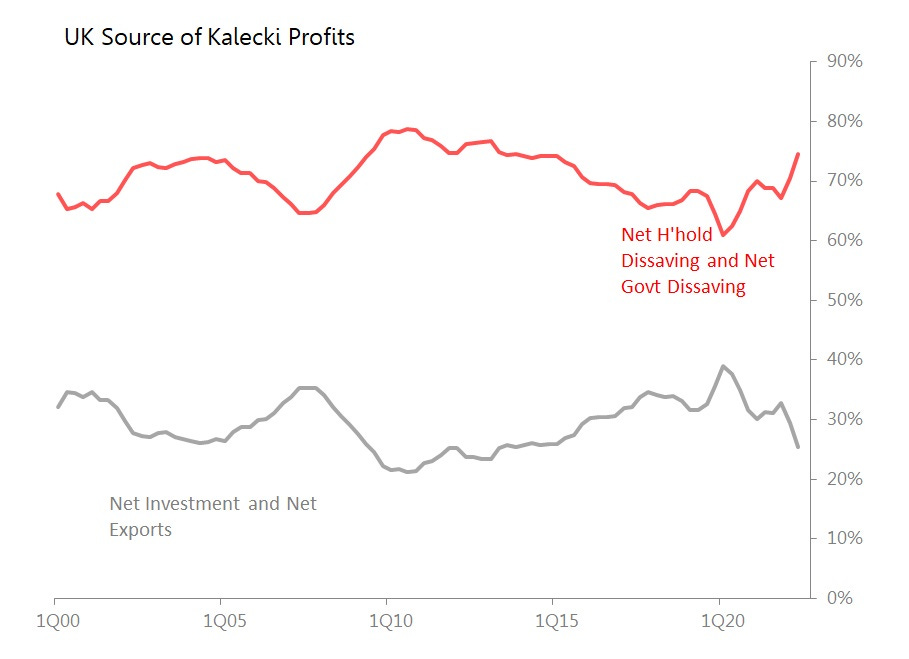

This is bad enough, but what is most alarming is the increasingly predatory way in which those profits are generated. These are ever-more tilted towards the dissaving of the household sector (accounting for 48% of the total in the 12m to June), and the dissaving of the public sector (accounting for 26.5%). Meanwhile, the combination of net investment and net exports - which, after all the measure of the productive and competitive components of economic growth - accounted for just 25.5% of profits.

The reliance for profits on household and government spending more than they earn or can raise in tax, is the most intense since 2013.

For those of you wanting the grisly details:

Household dissaving: in the 12m to June, household consumption rose 11.2% yoy, or by £38.3bn, but compensation rose only 6.1% yoy, or by £18.1bn, with the result that net dissaving rose by £20.2bn qoq, and in yoy terms rose £96.8bn. The rise in household dissaving was the single largest positive contributor to Kalecki profits.

The deepening household dissaving is also reflected in the deterioration of Britain’s net exports. In the 12m to June, the full trade deficit widened £28.6bn qoq and widened £65.1bn yoy. The chart strongly suggests a simple relationship between household dissaving and the trade deficit. That simple relationship is this: household’s ran down their savings, or borrowed, to spend money on imported goods and services.

Net investment, ie, the growth of Britain’s capital stock, was not a major contributor in the 12m to 2Q, rising only £7.7bn qoq and £22.4bn yoy. But even this is worse than it seems, because gross capital formation includes both business investment and household investment (ie, overwhelmingly, spending on housing). Whilst I estimate that Britain’s total capital stock rose 3.7% yoy, the stock of business capital rose only 2%. If so, the stock of business capital relative to GDP is now at its lowest since 2016.

Finally, the government’s attempts to retrieve the fiscal position it ruined during the pandemic (and which did so much to bolster corporate profits), is now a major drag on profits, with the 12m fiscal deficit narrowing £5.7bn qoq and £102.5bn yoy.

Altogether, this is a damning picture, with painful consequences.

The good news is that once we recognize the fundamental sources of our discontents, we stand a chance of rectifying them. And in fact, reformation of the British profits model is not impossible, nor need it be painful.

Next week, I will explain what needs to be done, and how it can be achieved, and make some concrete proposals for policies which can be implemented now, to start the change.